What is the 2024 forecast for the connector industry? What happened in 2023? What markets and industries saw the most growth, or the biggest decline? Is the West still outpacing the East in terms of connector sales growth? While we’re at it, what about connector prices and lead times?

Every few months we speak to our friends at Bishop and Associates and they provide insights and perspective on events in the $84 billion connector industry. Here’s their 2024 forecast, their 2023 year in review, and other observations and conclusions about an ongoing tumultuous year in the connector industry.

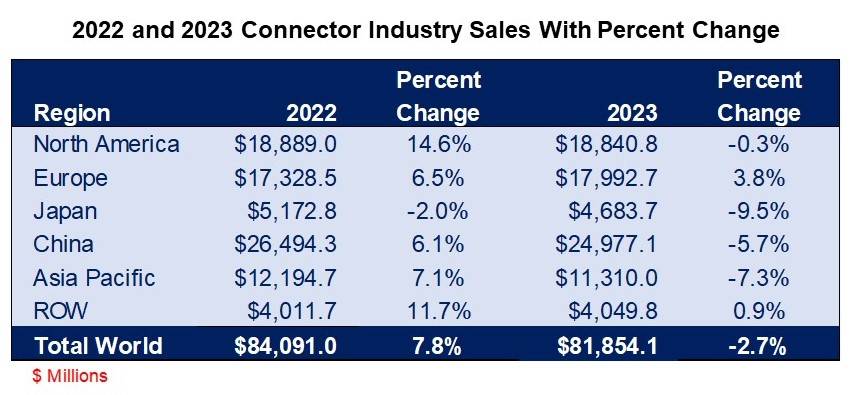

Danny: How did the industry perform in 2023?

Bishop: The world connector market declined 2.7% in 2023. In 2022 the industry shipped $84.091 billion versus $81.854 B in 2023. The table below identifies how the industry performed by geographic region.

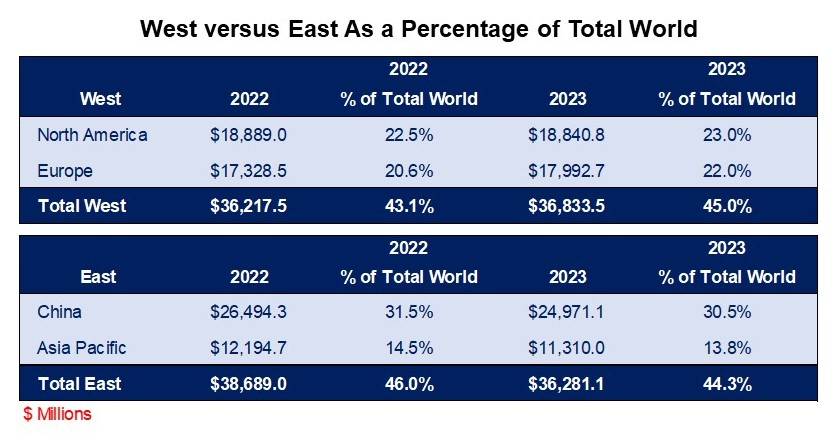

It is interesting to note that North America and Europe combined outperformed the combination of China and Asia Pacific.

This has happened for the past six years starting in 2018. It is also interesting to note that in 2023, the West shipped 45% of the world market while China and Asia Pacific shipped 44.3%.

Danny: How did the industry perform by market/end-use equipment sector?

Bishop: The table below identifies the performance by market/end-use equipment sector.

The worst-performing market sectors were computers & peripherals, consumer, and telecom/datacom. These were the hot markets during the pandemic. Stay-at-home workers, in the millions, upgraded their equipment, internet access, streaming system capabilities, smartphones, tablets, etc. This created a growth bubble in 2021 and 2022, which is now having an adverse impact on demand.

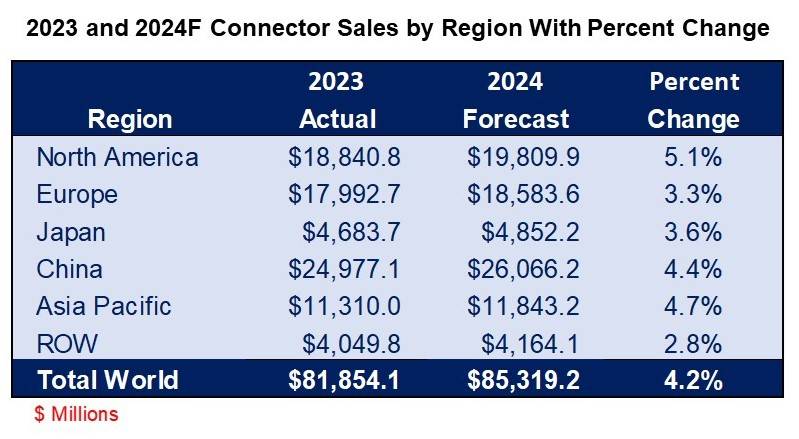

Danny: What is your 2024 for the industry?

Bishop: It is an election year in the US and for the European Parliament, so we anticipate several things could occur. In the US, we believe the Federal Reserve will hold interest rates steady or reduce them. Although inflation has come down, it is still north of 3% in the US, and just slightly below that in the Euro area. Worldwide gross domestic product (GDP) is at a reasonable level and is forecast to rise slightly going into 2025. With these factors in mind, we are reasonably optimistic and are forecasting the worldwide connector market to grow in the +4% range.

The following table shows our forecast by region for 2024.

We believe that North America will slightly outperform Europe, China, and Asia Pacific.

Once again, it is anticipated that North America and Europe combined (West) will out-ship China and Asia Pacific (East) in 2024.

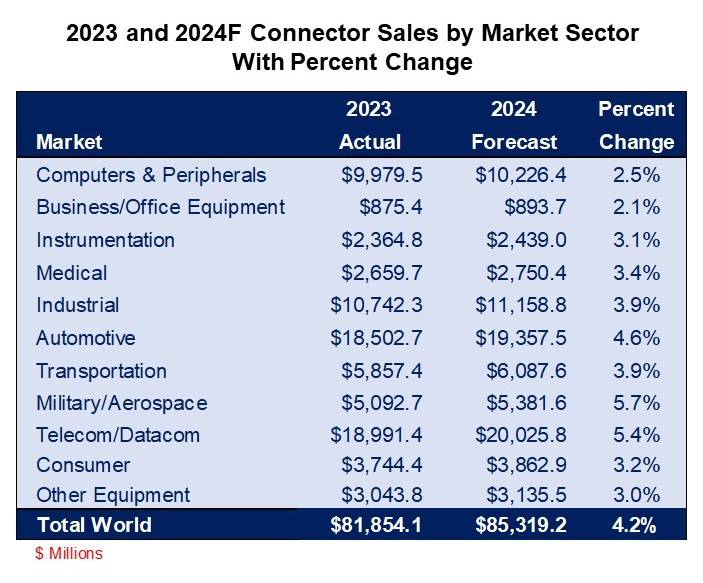

Danny: What market sectors will perform better than others?

Bishop: We believe automotive, and transportation will do well. We are concerned about the electric vehicle (EV) market because of slower consumer demand. As more people own an EV, we learn more about the downsides of electric vehicle ownership. The biggest is the lack of an adequate infrastructure to support its use, i.e., enough charging stations appropriately placed. Other issues include the ability of the battery to maintain a charge in cold weather climates and the risk of battery exposure to salt water in warmer coastal climates.

We also expect a good year for telecom/datacom. The Internet and the increasing demand for speed, bandwidth, etc. will fuel this demand.

The following provides our 2024 forecast by market sector.

The black swans are Russia and Ukraine, Iran, the Red Sea Turmoil, China and Taiwan, America’s southern border, and the increased potential for terrorism.

Danny: Yeah, those are some VERY black swans. Anyway, what are your thoughts on connector prices, lead times, the industry backlog, and raw material costs?

Bishop:

Pricing – We believe connector prices will remain stable in 2024. In 2023, customers pushed for price reductions because demand was lethargic (sales down 2.7% in 2023), inflation slowed down, and the cost of raw materials used in connectors stabilized. Customers will push for price concessions in 2024, but we believe manufacturers will be able to hold the line. We do not believe manufacturers will be able to increase prices.

Lead Time – Based on input Bishop has received, lead times are stable in the 8–12-week range. Of course, military/aero and some of your custom connectors are running higher, averaging 12 to 16 weeks. Bishop anticipates lead times to remain stable throughout 2024.

Raw Materials – Bishop predicts raw material costs will also remain stable in 2024. We measure and report on these costs each quarter. We don’t expect any surprises.

Industry Backlog – The connector industry backlog currently stands at 13.4 weeks. World connector backlog has been in the $21 to $22 billion range for all of 2023. We need to achieve a significant increase in order demand before the backlog grows. Unfortunately, we do not anticipate that happening in 2024.

Danny: Great stuff as usual. If a reader wants to learn more about the research, reports, and market data available from Bishop and Associates, what should they do?

Bishop: If you find this information useful, you may want to subscribe to our monthly newsletter The Bishop Report. To learn more about this month’s newsletters and the roughly 40 news briefs that are included in the subscription, visit www.connectorindustry.com to learn more. Or, you may e-mail Ron Bishop at [email protected] for a complimentary copy.

Danny (to our readers, not to the folks at Bishop): BTW, don’t forget that Samtec is still ranked #1 in Bishop and Associate’s Customer Service Survey of both North America and Europe.

Leave a Reply